SK Hynix: Chip prices increased by 20%!

On July 11, the media learned from the supply chain that Hynix has raised the contract price of DDR4/LPDDR4x by about 20%. This marks a new round of DRAM price increase trend. In the past six months, the price of DRAM represented by DDR4 has doubled. This price adjustment is mainly affected by the recovery of market demand and the adjustment of supply-side strategy, and is expected to further affect the cost structure of downstream electronic products.According to the EOL schedule of the original factory obtained through the previous supply link, Samsung completed the final order of DDR4 chips in June 2025 and completed the module shipment in mid-to-early December of the same year. SK Hynix estimates that it will stop accepting orders in October 2025 and complete the final shipment in April 2026. Micron notified customers in early June 2025 that its DDR4 will enter the EOL stage, and it is expected to stop shipments in the first quarter of 2026. After the three major memory original factories transferred all their production capacity to DDR5 and HBM, very little old process capacity was released.

It is worth noting that in the past June, with the announcement of Micron's suspension of production, the market's stockpiling sentiment accelerated and DDR4 prices were once pulled up.

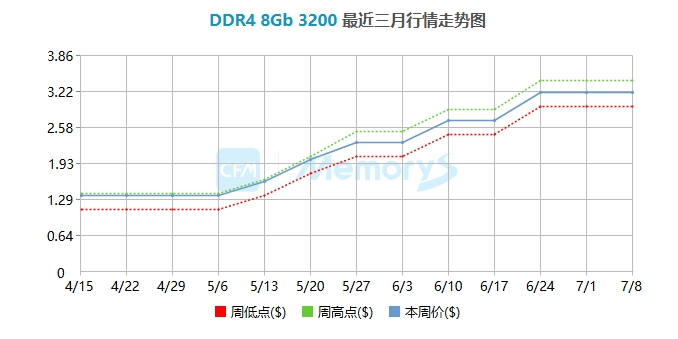

On June 13, DDR48Gb, 16Gb and other specifications rose by nearly 8% in a single day. On June 17, the spot price of DDR4 16Gb (1G×16) 3200 rose by another 6.32%, and DDR4 4Gb (512M×16) soared by 8.77%. On June 19, DDR4 related specifications rose by another 3.8%, and the increase was gradually fine-tuned, but the amplitude was still around 4%. After Micron announced the suspension of production, the price of DDR4 rose by nearly 20% in just a few trading days, and was even higher than the higher-specification DDR5 quotation, showing a "price inversion". Some industry insiders said bluntly: "I haven't seen such a large increase in spot prices in a single day for at least ten years."

However, after a whole month of skyrocketing, in July, market sentiment began to return to rationality, but the increase was still there.

On July 9, according to TrendForce's latest memory spot price trend report, DDR4 spot prices experienced a mild correction after a sharp rise. The flash memory market also pointed out that the server market is gradually returning to rationality, and the high-priced DDR4 RDIMM has caused the resistance of server end customers to become increasingly strong. Except for sporadic urgent orders, server end customers are generally unwilling to "take over" at high prices, and the overall trading atmosphere in the server spot market has become deserted.

Some memory manufacturers have realized that it is profitable to expand DDR4 production after seeing the price surge of DDR4 in the short term. After the news came out, the prices of some DDR4 modules also fell slightly.

However, as SK Hynix raised the contract price of DDR4/LPDDR4x, the short-term price of the storage market may still be high.

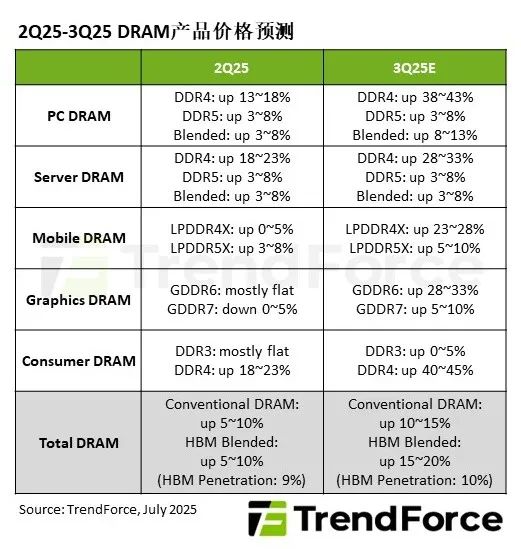

TrendForce also stated that the demand for DDR4 continued to be hot in the third quarter, and the original manufacturer intended to increase the price increase. In the case that the manufacturer's production capacity cannot be fully connected, and the capacity of some manufacturers' products is small and cannot meet the specifications of customer requirements, DDR4 will still be in short supply in the short term. In the third quarter of 2025, the price of conventional DRAM will increase by 10% to 15% quarter-on-quarter. If HBM is included, the overall DRAM price increase will increase by 15% to 20% quarter-on-quarter.

In addition, because DDR4 currently prioritizes server demand, the supply for consumer applications is limited, and the scale of consumer orders is small, buyers lack bargaining power, and it is expected that the price of consumer DDR4 will increase by 40% to 45% quarter-on-quarter in the third quarter.